Officials discuss advantages and challenges of such a project

An Austin development team is helping tackle the housing crisis by converting hotels into apartment complexes.

Shir Capital and Pfluger Architects have completed a number of hotel-to-apartment conversions in Austin, Houston and Colorado in recent years, and they’ve now converted a North Austin Quality Inn at 7928 Gessner Drive into an apartment complex they’re calling the Veer Apartments.

The design and layout of hotels make them better candidates for conversions to apartments than office buildings, said Erik Leitner, principal at Pfluger Architects.

“This was a concrete building, so it had very strong bones to be able to adapt,” Leitner said. “It was already a hotel, and when converting those into an apartment building, that layout is pretty much started. The plumbing is already laid out there, so it’s convenient for us to use those existing systems. And, we don’t have to knock the building down. It’s cheaper to renovate that building than it is to build new.”

The construction budget for the project was about $12 million, said Elan Gordon, principal at Shir Capital.

The Veer Apartments has 174 studio apartments that began as roughly 120 hotel rooms, Leitner said. While the hotel rooms themselves all became apartments, the development team also was able to utilize the open space of the hotel’s atrium to create an additional 50 apartments “out of thin air,” he said.

One of the biggest challenges of such a project is figuring out a plan for mechanical, electrical and plumbing elements, Leitner said. Major considerations for the development team included determining if the hotel had sufficient water capacity for additional units and kitchens on top of the existing bathrooms, and if there was enough electricity to power appliances. In the end, they added new electrical service to the building.

Shir Capital purchased the building during the Covid-19 pandemic, Gordon said, and one of the factors contributing to the decision to renovate the property was the lack of hotel traffic at the time.

“That was certainly the dollars and cents of it,” Gordon said. “But Shir Capital is not traditionally a developer. Really, it’s an owner and operator of apartments, so if we’re going to go develop apartments, let’s have something that’s three-quarters done already … it is in all cases kind of simpler than doing ground-up (development).”

The notion of converting vacant office space into apartments has been bandied about nationally in recent years, based on high office vacancy rates and the need to create more housing. But Leitner said converting office space is considerably more difficult than hotels.

For one, office buildings are typically built with central banks of restrooms. In apartments, however, individual plumbing fixtures are needed in each for sinks, toilets and appliances.

“You’ve got, let’s say, one kitchen and two bathrooms on the whole floor for an office building, right?” Gordon said. “We started with 25 bathrooms (per floor), and we added the kitchen in this case, but we already had all of that plumbing and the kitchens are piggybacking off of the plumbing that’s already there.”

Another consideration is that, unlike many offices, the walls for apartment units are already in place when a hotel is converted.

Overall, the Veer Apartments project took around four years to complete, from the acquisition in late 2020 to completion in late July this year. Although hotel traffic was slow during the pandemic, Shir Capital continued to operate the property as a hotel for nine months to a year while working on design and permitting for the conversion, Gordon said.

Construction took two to three years. Gordon noted that one issue that can cause delays in such conversions is that original design plans for older properties are often unavailable, mandating that developers measure and re-measure multiple times and conduct re-designs throughout the process as they discover new information.

“That’s all part of the process of these older hotels getting to the promised land,” Gordon said. “It feels like you’re three-quarters done when you show up, but you find out that last quarter is way more complicated than you might think because there’s a lot of stuff that gets done without permits, or was patchworked over the years.”

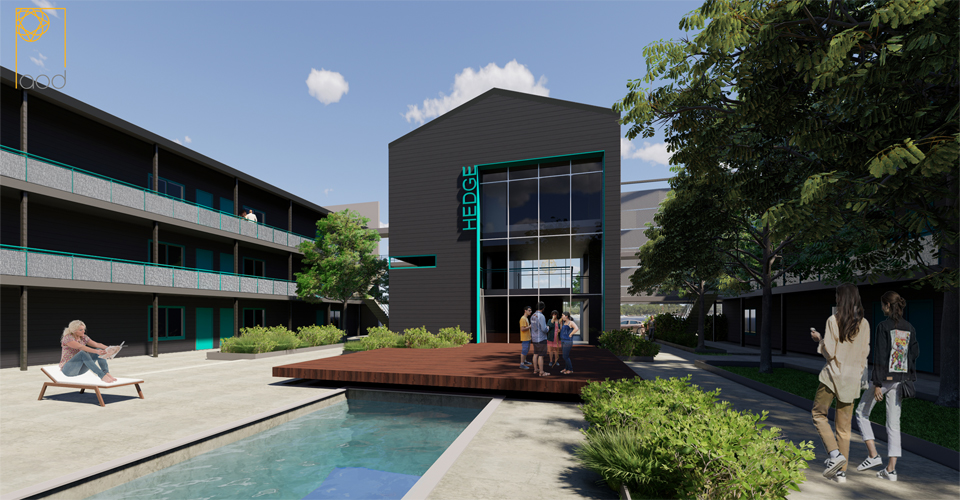

Shir Capital and Pfluger Architects have collaborated multiple times now on hotel-to-apartment conversions. The companies completed North Austin’s Hedge Apartments and Alma Apartments in 2024, the Teak Living apartment project in Houston and Alta Living in Colorado Springs, Colorado.

It’s not a typical cycle. That much was agreed upon at Commercial Observer’s real estate investment forum on April 18 at the Santander Tower in Downtown Dallas.

Katy Carmical, partner with Hunton Andrews Kurth, moderated a panel discussion on the changing investor landscape in the U.S., and talked about what it’s like to work in today’s market. Tony Fineman, senior managing director and head of originations at Acore Capital, said there is far more capital ready to be deployed than there are deals looking for financing.

“We’re flush with capital and want to put it out,” he said. “Sometimes, where we want to put it and where the borrower wants it is not the same. But, we’re a little bit agnostic in that we just need trades to happen.

“For two years, I’ve been saying the issue in the lending business is we need to further acquiesce to the fact that interest rates are where they are,” Fineman added. “Interest rates impact value, and when a buyer and seller — or a borrower and lender — agree on what the value is, then a trade can happen.”

Sondra Wenger, senior managing director and head

of commercial real estate for the Americas at CBRE Investment Management, said it’s important to be able to pivot and respond to market trends and research. She pointed to work from home trends resulting in far fewer trips to central business districts for errands or lunch. Instead, people are visiting neighborhood retail centers at greater rates than before the pandemic.

“If you look at that from a high level, there is limited supply, they have high occupancies, and there’s a lot of under-market rents making it a really attractive investment today,” Wenger said of neighborhood retail properties. “Because retail was in the doghouse for the last nine to 10 years, there wasn’t a lot of construction getting done. So the supply did not keep up with the demand. It didn’t even keep up with population growth.”

She said, despite negative sentiment, CBRE has seen the highest occupancy levels in retail in the last 24 years, and retailers are seeing higher consumer spending per square foot when compared to recent averages.

“We expect that trend to continue on for the next three to four years,” she said. “Because rents were not moving up due to people’s fear of retail, there’s a real mark to market growth in your rental rate. … It’s also unique in that you can get positive leverage today on most of your retail deals.”

Mark Roberts, managing director of research at Crow Holdings Capital and also at the SMU Cox Folsom Institute for Real Estate, said while it’s not a typical cycle, there is a lot to be optimistic about. He said investors are responding to the state of money markets by reducing exposure in the stock market and targeting assets with good yield.

When it comes to U.S. office real estate, Wenger said the market tells a bifurcating story between top-shelf space and everything else. “It’s a very different animal,” she said. “There is a much wider spread in that bid-ask for the have nots versus the haves.”

She said the haves in the office market are actually seeing rent growth and some of the lower vacancies. “We’re seeing a huge trend where tenants are now using this as an opportunity to say, ‘We want to get into some good space where we can really pull our tenant pool and our workforce in,’” Wenger said.

Roberts said it’s a tenants’ market, which means it’s going to take a lot more capital to develop leading office amenities. “Part of the challenge is that not all landlords are well capitalized to do it,” he said.

Wenger added that funding is the first thing office tenants ask about when touring properties. “It’s not ‘Where’s the metro line?’ or ‘What amenities does this building have?’” she said. “We’re now getting asked, ‘What is the capital stack of this building?’ because it’s very important for tenants to know if they’re going to make a commitment that it’s not going to turn into a zombie building.”

Opinions from the panel about multifamily investment were varied. They agreed, though, that multifamily operation fundamentals remain strong.

“Most of the properties you see that are distressed aren’t distressed because the occupancy is not there,” Jay Porterfield, executive director at PGIM Real Estate and another panelist, said. “They’re distressed because of the financial engineering that went into the capital stack. My living is made around apartments, so maybe I’m biased, but I continue to be bullish on apartments. But you have to pay the right price.”

Wenger said CBRE was expecting distress in the multifamily market because of the volume of deals completed in 2021 and 2022 at very low cap rates. “But the reality is, there just isn’t yet because it is a long-term investment asset class,” she said.

Fineman cautioned that the nation isn’t out of the woods when it comes to multifamily distress.

“If the [U.S. 10-year treasury] stays at 3.5 to 4 percent, distress in multifamily is coming up,” he said. “There will be capital that’s dejected by the current owner, or capital dejected by the next owner. I think there’s tremendous opportunity and we’re very bullish on putting money out in the multifamily market. But to say we’re past seeing distress in multifamily is not correct.”

Colin Fitzgibbons, president at Hunt Realty Investments, said he’s optimistic about multifamily, and the company is working on affordable and workforce housing projects. He pointed to Downtown Dallas’ deficit in affordable housing.

“It is a problem, and it’s going to affect the overall growth if we don’t figure out a way to address it,” he said. “So I’m someone who spends a lot of time trying to wrap my mind around how the numbers work, but we’re very bullish on the long-term prospects.”

Most of the panel said places like Dallas are prime targets for investment thanks to favorable business and political environments, and to persistent in-migration. “The key thing to us as we look at other markets in this country where the policies of the government are anti-growth, anti-investment; look at Dallas and Texas: People are still moving here. There’s still migration into this city,” Fineman said. “The truth is these markets are resilient. The growth is fostered here. So we’re really bullish on lending here. Wegner said CBRE’s recent investor intention survey showed Dallas ranked as the top market in the nation in terms of places that companies want to invest in more.

Carmical wrapped the panel by asking for bold pre- dictions for 2024. “I don’t think the Fed moves [interest rates], and I think the treasury stays where it is right now,” Porterfield said. Fineman predicted one rate cut this year “right before the election.”

Roberts’ forecast shows a lower chance of cap rates rising then falling over the next couple of years. Wenger said there will be an undersupply in “brand-new responsive office space in 2025.” And Fitzgibbons predicted “more new office development than you think.”

In a separate panel, Michael Cohen, founder of Brighton Capital Advisors and an expert in CMBS and CLO financing, discussed his firm’s business of usher- ing borrowers through the new post-pandemic era of loan servicing and distress on the capital markets side of commercial real estate.

“CMBS is effectively going to a pawn shop where it’s stacked against you,” Cohen said. “The headlines are true: Borrowers do not have power with these special servicers. Once you get into special servicing, you’re going to start to incur fees. And you’re under their control.”

He anticipates more distress on the horizon, particularly in the multifamily sector, which will require a lot more restructuring, extensions and other solutions. “There’s no dramatic interest rate change that’s going to come that’s going to save everybody,” he said.

CO’s Dallas investment forum had started with a keynote by Christopher Ludeman, CBRE’s global president of capital markets, with Scott Durco, an Acore managing director and head of its central region originations. There was also a panel on lending that Katherine Tapley, a partner at Norton Rose Fulbright, moderated. It included Adrienne Bain, capital markets managing director at JPI; Tom Burns, a managing director at Affinius Capital; Scott Gosslee, senior vice president and Texas market executive at BankUnited; Lee McCormick, president of Lone Star PACE; and Sean Ribble, senior director of originations at Nuveen Green Capital.

A panel on multifamily development included moderator Katie Van Dyk, a partner at Norton Rose Fulbright; Joel Behrens, managing director at Trammell Crow Company and High Street Residential; Harry Blanchard, managing director at Vichara Technologies; Nadia Christian, a partner at Wolverine Interests; and Claudia Powers, managing director at Acron USA. There was a keynote talk, too, between Hines’ Ben Brewer and Fawaz Bham of Hunton Andrews Kurth. And a panel on affordable housing in Dallas with James Armstrong from Builders of Hope CDC; Ashley Brundage of United Way of Metropolitan Dallas; SHIR Capital’s Elan Gordon; and Avanath Capital Management’s Wesley Wilson, who moderated it.

A Los Angeles-based developer is giving new life to a shuttered Hilton Hotel in Houston.

Bryan Kang’s Dos Lagos Asset filed documents detailing plans for adaptive reuse of the former 292-room Hilton Houston Galleria at 6780 Southwest Freeway. A multifamily complex is planned, but the number of units wasn’t included in the filing.

Conversion of the 200,000-square-foot, 13-story building has an estimated cost of $40 million. Dallas-based design firm Huitt Zollars is attached to the project. Construction is expected to start in April, with an estimated completion date in September 2025.

Kang was commissioner of the Los Angeles Department of Transportation from 2012 to 2014 but has since turned to the world of real estate.

In 2019, he purchased an office building in Orange County for $13.4 million, according to Traded LA. Before joining politics and real estate, Kang was the CEO of the wholesale merchandiser Rhapsody Clothing, which sold to stores across North America, as well as South Korean retailer Home Plus. Rhapsody Clothing closed in 2019, according to California business records. Attempts to reach Kang were unsuccessful.

Originally constructed in 1978 and remodeled in 2016, the Hilton Houston Galleria has been vacant since its lender foreclosed on the property in 2022. The hotel had closed because of the pandemic. It remains real estate-owned, according to the Harris County Appraisal District. Its 2023 assessed value was $7.2 million.

Hotel-to-resi conversions are a burgeoning business in Houston’s commercial real estate scene. As the Bayou City’s hospitality market has seen deflation post-pandemic, as depressed occupancy rates and loan delinquencies shake the market. Trepp ranked Houston’s hotel market as the nation’s worst last year.

While office-to-resi conversions make the headlines, hotel-to-resi reuse developments comprise 58 percent of Houston’s conversion market, according to RentCafe.

The Houston Housing Authority, in collaboration with Columbia Residential, is converting a dilapidated Holiday Inn at 2100 Memorial Drive, long an eyesore near Buffalo Bayou, into an affordable 197-unit senior living complex.

Hotel-to-resi developer Shir Capital acquired the defunct Wyndham Hotel at 14703 Park Row in 2022. It is planning to open Teak Living, a rental community, by the end of this quarter.

April 30, 2023 | Maddy McCarty, Bisnow Houston (mailto:maddy.mccarty@bisnow.com)

If the Alamo was in Houston, Houstonians would’ve torn it down to build something else.

So says Ori Batagower, new development and acquisitions director for The Deal Co., one of several panelists at Bisnow ’s Houston State of the Market event April 27 to proclaim that razing is out and a new era of adaptive reuse is in.

Bisnow’s event was held in a raw space at 1512 Center St., the original 1927 Bosworth Paper Co. building that The Deal Co. is redeveloping — a fitting symbol of changing mindsets in a city known for no hesitation when it comes to chucking out the old and making way for the new.

Batagower and others agreed more Houston developers are slowly seeing the value in restoring old buildings. But panelists warned such projects are not always straightforward.

“Every single step that seems to be pretty typical for different classes of real estate is not [for adaptive reuse],” said Andrew Nurcahya, who is developing The Dryer in Katy.

The Dryer is a 177-foot-tall former rice dryer along Interstate 10 in Katy, still the tallest building in the city and the visual that many residents rely on to know they are close to home, Nurcahya said. It was built in 1943 and has been abandoned for more than three decades.

Adaptive reuse projects like The Dryer are difficult due to numerous challenges, including unexpected construction costs and a lack of permitting guidance for one-of-a-kind projects. Layered on top of that are the conditions looming over all of Houston’s commercial real estate market: high interest rates, a lack of ideal inventory for tenants, a disconnect between sellers and buyers, and a lack of financial liquidity.

Nurcahya embodies the qualities of those willing to develop this type of project, or, as he put it, “I’m just the crazy person that’s taken it on. “He hopes that turning it into a family entertainment venue and allowing the public to touch and experience the building again will have a great impact on the community, casting the project as a labor of love.

“My project is probably the most extreme out of a lot of the projects here. A lot of your projects here actually economically make sense, there’s an ROI component there,” Nurcahya said, indicating that his doesn’t and garnering a laugh from the crowd.

To date, Nurcahya has dealt with issues like finding underground gas pipelines with no official documentation and difficulty securing financing.

“Underwriters don’t look at the cool, fun factor that we first look at, they look at the fear factor,” Nurcahya said. “Ori has said, it’s not for the faint of heart. But it certainly is a cool project.”

No one will believe in a project as much as you do, Buffalo Bayou Partnership Real Estate Project Manager Ian Rosenberg agreed. Taking on adaptive reuse projects means accepting a higher level of risk and being willing to make judgment calls, he said.

“Bankers are risk-averse, engineers are risk-averse, city permitting is definitely risk-averse,” Rosenberg said. “They don’t share your passion. They love the design, but they’re not going to risk something … So [you’re] dealing with that risk, from go [and] all the way through a project.”

Many of those risks are impossible to mitigate before starting an adaptive reuse project, Batagower said. Peeling back the layers on old buildings — like the century-old building The Deal Co. is redeveloping at 2103 Lyons Ave. that will house a Meow Wolf location — is fun, but not to be undertaken by a group without experience, he said.

“You have to get started and just believe in what you’re doing. And then you’ll figure it out along the way,” Batagower said.

Figuring out how to finance projects is a major hurdle for both developers of older buildings and commercial real estate writ large, and brokers, sellers and others are getting creative to push deals to completion.

Acho Azuike, chief operating officer and managing director at DC Partners, said he did a pulse check with lenders a few weeks ago, and some people and asset classes are “getting shy.”

That’s requiring more tapping into alternatives like EB-5 financing, Property Assessed Clean Energy (PACE) financing and crowdfunding, he said.

“We’re hoping to get as creative as possible and looking at financial tools that we’ve never used in the past,” Azuike said.

In the multifamily market, options to get deals across the finish line include accepting lower returns and lowering sale prices, Barvin Senior Vice President of Acquisitions Susan Pohl said.

Tenants are willing to pay a little more on rent, so eventually, developers might have to accept doing business at a 10% interest rate, SHOP Cos. partner Chris Reyes said.

“Like we were doing in the ’80s and ’90s,” he said. “I think once people come to that reality, we’ll be able to solve problems. Because, at least on the tenant side, we’ve shown that …we’re good with paying a little more red if that’s what it costs to create more opportunity.”

But Pohl said she imagines something closer to a 4.5% interest rate is needed to get things moving. Sellers may be interested in selling at a 4% cap rate, while buyers can be interested in getting debt at a 4% or 4.5% rate. That would mean a little negative leverage for a short time, she said.

“I think it’s going to have to get to that level to bring buyers and sellers together,” Pohl said.

The economic environment might cause some to try to wait for better conditions to make deals, but CBRE Vice Chairman Lucian Bukowski said “deals have an expiration date,” and called on leaders to lead.

“In a lot of cases right now, they’re putting things on hold,” Bukowski said. “Leaders don’t get paid a lot of money to do nothing. They get paid to make the important decisions that drive them toward the future.”

March 31, 2023 | 5:30 AM SHIR Capital identified the former Hotel Elegante in Colorado Springs, now ALTA Living, as a candidate for conversion to multifamily, an ambitious plan that earned it CoStar’s 2023 Impact Award for best redevelopment.

A panel of local judges familiar with Colorado Springs’ real estate industry chose the project because of its purpose and large scale. Hotel Elegante had 496 hotel rooms and more than 60,000 square feet of amenity space, making it the third-largest hotel in the state during its heyday. Its transformation into apartments qualifies as one of the largest hotel to multifamily conversion projects in the U.S.Most importantly, the conversion will deliver an affordable housing option to the Colorado Springs market that has seen record rent increases, and should cater to the large military presence in nearby Fort Carson.

About the project: SHIR partnered with The Valcap Group to design and carry out the conversion. To date, 200 units from the former Hotel Elegante have been upgraded,providing 501 affordable housing units.

What the judges said: “This is good affordable housing option to support the military and market needs of southern Colorado Springs,” said Austin Wilson-Bradley, economic and community development manager for the Downtown Partnership of Colorado Springs.”ALTA achieves many community goals such as adaptive reuse and infill as well as increasing the supply of multifamily housing with a goal towards affordability,” added Paul Morrow, a senior analyst with city of Colorado Springs’ community development department.

Who made it happen: Elan Gordon, principal of SHIR Capital, and Richard Fishman,president and founder of Valcap Group, along with Zachary Streit, founder and managing partner of Los Angeles-based WAY Capital.

CoStar’s Impact Awards highlight the commercial real estate transactions and projects that have transformed their markets over the past year. The winners are chosen by independent panels of industry professionals who work in the markets they judge. Learn more about the awards here.

In May 2021, Principals of SHIR Capital & Valcap closed the the sale of Nextloft Apartments in Bluffton, SC for $18.15 Million, yielding a 50%+ IRR. Principals of SHIR acquired a 148-unit extended stay hotel complex in January of 2018 for $7.25MM. Starting with a fully vacant hotel, SHIR’s construction affiliate Ava’s quickly renovated all interiors and began move-ins in only 6 months. SHIR’s property management affiliate Nexus leased the property to stabilization in 12 months and maintained occupancy and collections throughout 2020’s pandemic with physical occupancy above 97%.

After purchase, a full value-add renovation was undertaken improving and adding to the amenities, along with strategic cosmetic exterior upgrades, including:

Redesign of pool

New leasing office

New landscaping

Barbecue area

Exterior lightning

Re-branding & signage

Parking lot upgrades

Interiors for all of the residential units were upgraded including:

Investors are buying hotels and turning them into rental apartments, in the latest sign of how the Covid-19 pandemic is changing the American real estate market. These buyers are trying to take advantage of the hospitality industry’s crisis by taking over struggling or foreclosed properties at bargain prices. They are also looking to profit from rising demand for cheap housing from households forced to downsize during the recession. The small but growing number of hotel conversions some properties are also being turned into offices-is a symptom of the turmoil the pandemic has caused in the hotel sector. Many properties are shut down or running steep losses because of a drop in travel.

The share of hotels with securitized mortgages that were delinquent on their loans was 19.66% as of November, up from 1.52% a year earlier, according to Trepp LLC. Even before the pandemic, a surge of hotel construction over the past decade had left some cities with a room glut.

”We consider ourselves a building recycling company,” said Dan Norville, president of Vivo Living. The company converted its first hotel into apartments in late 2019 with the former Bigelow hotel in Ogden, Utah, a property originally built in 1927 with about 112 rooms.

Since the start of the pandemic, Vivo has added three more hotel conversion projects in Mesa, Ariz., South Bend, Ind., and Winston-Salem, N.C. The company is in contract to buy a fourth hotel, outside San Antonio early next year. Many of the properties Vivo is looking at are older motels with open-air corridors and staircases shunned by big hotel brands. ”There are so many of these exterior-corridor motels throughout the U.S., and it’s a functionally obsolete product type for the hotel industry,” Mr. Norville said. ”But when you look at them, and you look at a garden-style multifamily right next to it, they’re almost the exact same property footprint and type.”

Elan Gordon, principal of real-estate investment company SHIR Capital, which has converted hotels into hundreds of apartments in South Carolina and Texas, said the business plan works best in markets where the price of studios in new buildings has crept over the $1,000 a month mark. Hotel-room-sized studios can compete with those apartments with a 20% discount on rents. ”We are working within the market circumstances to kind of solve an affordable housing problem, even though it’s not our business plan to create affordable housing,” Mr. Gordon said.

Extended-stay hotels are ideal for creating the cheaper apartments, Mr. Gordon said, because while they typically measure smaller than the average apartment, they already have bathrooms and kitchenettes built into them. More conventional hotels need a more expensive rebuild, but even that often takes less than a year and is much faster than building from the ground up, investors say. Since the pandemic began, Mr. Gordon is in contract to convert a conventional hotel in Austin, Texas, into apartments, having previously finished three others.

These conversions sometimes require zoning changes that can be time intensive. Mr. Gordon said he has accomplished this in some locations by demonstrating to local governments that his apartments would be among the most affordable in the market. In many cases, hotel rooms are just large enough to qualify as the smallest housing units allowable under zoning law, said Jonathan Needell, president of real-estate investment firm Kairos Investment Management Co., which has lent money to converters.

Austin has been a particularly hot market for converters. The city has an average rent of about $1,500 a month, according to data from Yardi Matrix, a level that makes it difficult for many young professionals to have places of their own. ”The whole millennial thing of spending 40% or 50% of your income on rent, it just doesn’t make any sense,” said Lee Stuart, a 32-year-old concert promoter who lives in a 300-square-foot studio at the Hedge, a former hotel north of downtown Austin. Mr. Stuart was particularly budget conscious this spring when he was apartment hunting because he was furloughed early in the pandemic. The $700 rent is much cheaper than the typical apartment in his neighborhood. His plan is to use his savings from the lower rent to buy his own place eventually. ”If I do this for a year or two … I could go buy a two-bedroom apartment or condo” he said.

Isaac Kassirer was at the forefront of one of the hottest trends in commercial real estate. He borrowed from global investors by promising to gentrify apartment buildings in New York’s low-income neighborhoods and raise the rents. Mr. Kassirer fell behind on some loans before the coronavirus pandemic and now some tenants are in open rebellion. Longtime residents, joined by some new, high-paying renters, are on strike. When the pandemic ends, recently passed pro-renter laws are likely to make it harder for him to carry out his plan.

Mr. Kassirer’s company, Emerald Equity Group, said that “these issues we are experiencing in fact what many building owners in this great city are finding themselves grappling with as a whole” and that it is addressing tenants’ complaints. Wall Street embraced landlords like Mr. Kassirer over the past decade. Bankers packaged up their loans and sold them to bond investors with the promise that the buildings would generate much higher income. The market for those bonds grew from about $400 million of issuance in 2012 to $22.4 billion last year, according to commercial mortgage tracker Trepp LLC. Rental housing was the most common property type financed by such bonds. Today, the combination of new laws meant to preserve low-income housing and the pandemic has left many of the borrowers struggling to pay off their debt. Forbearance programs tied to the pandemic are delaying a possible reckoning. Mr. Kassirer borrowed $90 million from global investors in late 2018 to upgrade nine buildings he owns in New York’s East Harlem neighborhood.

Emerald promised to realize a “strategic vision to replicate the high-class Manhattan amenities,” according to its website. He had fallen behind on some mortgage payments before the pandemic hit and about 40 of his mortgages in the area went into forbearance in the spring, according to Freddie Mac data. The $90 million mortgage he got was called a transitional loan. Transitional loans are riskier than typical commercial mortgages advanced by banks. The space is dominated by nonbank lenders such as credit funds and real-estate investment trusts that have grown to become a major force in commercial real-estate finance in recent years. They originated an estimated 12% of commercial mortgage loans by value in 2019, up from 2.9% in 2009, Mortgage Bankers Association data shows. Mr. Kassirer got his transitional loan from LoanCore Capital, a lender owned by two of the world’s biggest investors, Singapore’s GIC, a sovereign-wealth fund, and the Canada Pension Plan Investment Board. The two investors together manage more than $700 billion. The Singaporean and Canadian funds deferred comment to LoanCore. A spokesman for LoanCore said the company is a responsible lender that takes strong actions to remedy issues faced by tenants in buildings it financed. The company didn’t provide examples of any actions it has taken and the spokesman declined to comment further.

East Harlem has long been home to low-income, Spanish speaking residents. It is where Magdaly Marrero, 60, raised her two children on paychecks from McDonald’s, KFC and Popeyes restaurants. Mr. Kassirer bought her building in August 2017, shortly after he purchased several dozen similar buildings nearby, totaling nearly 1,200 units. It was the biggest deal yet for the then-34-year-old real-estate investor who had previously bought buildings in the Bronx. LoanCore packaged Mr.Kassirer’s loan with dozens of similar mortgages into two bond deals totaling $1.5 billion.

Transitional loans, which were popular in hot real-estate markets such as California, Florida, New York and Texas, did create affordable housing in some instances. Elan Gordon used transitional loans to convert two struggling hotels into 240 affordable apartments in Greenville and Bluffton, S.C. “It’s delivering new supply to an area that needs it,” said Mr. Gordon, who runs SHIR Capital, an investment firm in Austin, Texas. He is converting four more hotels in Austin into below-market rent apartments.

In other situations, the loans are used to boost rents. In Toledo, Ohio, one bond funded a $23 million loan on 888 apartments where the owners planned to introduce regular rent increases, pet fees, application fees and eliminate free housing for maintenance staff, according to a prospectus. In the East Bay of California, a formerly seniors-only community is in the midst of a conversion to an all-ages apartment complex. Current rental listings suggest the property owner is making good on its plan to increase base rents by 64%, as projected in a 2018 bond prospectus. Banks cut back on transitional lending for reputational and financial reasons. “It’s just not our business model,” said Joe Fingerman, head of commercial real-estate lending at Signature Bank, a New York lender. The bank backed off from such lending under pressure from affordable housing groups. The bond market that financed transitional loans sputtered this spring when the pandemic hit. The share of delinquent loans increased from 0.22% in March to 2.2% in September, Trepp data show. New deals also slumped, with about $7 billion of new issuance so far in 2020, versus $22.4 billion for all of 2019. Half of the 2020 volume was before the pandemic, according to Trepp. Hit by New York’s new rent laws, pushback from tenants and the impact of the pandemic, Mr. Kassirer’s situation is worse than for most landlords. Tenants say he let his buildings fall into disrepair. Rat and cockroach infestations, mold, broken radiators and appliances, gas shut-offs and other issues have forced some tenants to move. Others stayed put and joined the rent strike in East Harlem and three other Manhattan properties where tenants are collectively withholding more than $600,000 of rent checks, according to those tenants’ attorney. Emerald said that the issues inside the buildings “were not caused by us but rather [were] the result of aging structures built at the turn of the last century that are in need of restorations and upgrades.” It added that it is making “strenuous efforts to address any outstanding issues at our buildings and are confident of resolving these soon.”

As the pandemic ravages the hospitality industry across the country, forcing hotels to close and lay off thousands in the Austin area alone, at least one Austin-based real estate investment company sees opportunity.

SHIR Capital is shifting from buying apartment complexes with value-add opportunities to buying hotels that it can convert into affordable, micro-unit apartments. The company seeks to buy 10 to 20 hotels in prime areas across the country. It’s a niche that SHIR Capital tapped into prior to the pandemic, but one that could grow within the next six months to two years as more hotel loans go into default due to the downturn in travel.

“Coronavirus comes then hotels take a huge hit, and now it is our primary focus,” said Elan Gordon, principal of SHIR Capital. “It is where the deals make sense for us, price point wise. On top of that, if it is in the right area it often makes sense.” This strategy will also add hundreds if not thousands of much-needed affordable apartment units — renting at around $800 a month — to Austin, he said.

The city of Austin is also buying and leasing declining or closed hotels to serve as homeless and domestic violence shelters.

Charles Cirar, vice chairman at CBRE Group Inc. specializing in multifamily, said his office has been fielding calls from investors looking for similar opportunities amid the pandemic. “We believe this redevelopment strategy has considerable potential, but also see it as a limited niche play that will likely not have a significant impact on either the overall hospitality or multifamily markets,” he said. Investors are targeting limited-service hotels that they could buy for between $20,000 and $30,000 per room key, Cirar said.

Gordon said his company has partnered with funds on both the debt and equity side to acquire hotel properties on a “price per pound” based on the number of units rather than based on its net operating income since these properties aren’t generating much if any revenue right now. Many hoteliers are looking to get out of the business because it may take a few years for revenue to rebound, he said. Others are delinquent on their mortgage and want to sell before the bank takes the property.

Gordon said his company is calling hotels along I-35 and tracking hotels that have loans that are maturing or defaulting. They are also buying hotel loans and picking up properties on the auction block.

Because of the strength of the Austin economy, Cirar said he doubts whether a large volume of hotels would be sold at the price level needed for these apartment conversions in Austin. In many cases, the underlying value of the land would offer greater potential for new multifamily development, particularly in more infill locations, he said.

Potential pitfalls for projects of this type are obtaining financing for the conversion and making costly mistakes in the renovations, he said. Joe Dowdle, senior director of multi-housing advisory at Jones Lang LaSalle Capital Markets, agreed that hotel conversions could be a short-term niche.

He said investors face many challenges as hotels can generate more revenue by renting rooms at a nightly rate versus a monthly apartment rental rate, and many hotels are encumbered by franchise agreements that could last 15 to 20 years. Termination of these agreements could mean substantial fees.

When looking for potential hotel properties to redevelop, Cirar said investors should look for what they would in a new development site such as visibility and safe ingress/egress from well-traveled roads, walkability to conveniences, access to entertainment and recreation and parks, proximity to employers, and desirable schools and neighborhoods. “Many existing hotel properties in Austin, both urban/infill and suburban, do check all or most of these boxes,” he said.

Austin Projects

SHIR Capital’s first Austin hotel conversion is at the former Austin Suites Hotel at 8300 N. I-35 that it bought from Artesia Real Estate in March. Artesia had bought the closed hotel in 2018 with the plan of transforming the 215 rooms into apartments.

According to its website, SHIR Capital bought the property for $9.5 million and plans to invest about the same amount in improvements. Travis Central Appraisal District values the property for tax purposes at $6 million. The process of renovating the extended stay hotel, now dubbed The Hedge, has begun and some tenants will even be moving in soon, Gordon said. The pool, fitness center and other amenities are being updated as well as SHIR seeks a mixed-use overlay zoning from the city for the property and works to bring the property up to code. Austin Outdoor Design is working on the project.

All units at The Hedge will be studio apartments of about 275 square feet each. They are leasing for about $750, but Gordon said he expects that price to rise because of early demand. Other studio apartments in the area such as Orbit, Starburst and Centro are leasing for more, between $800 and nearly $1,000 a month.

Prior to this project, SHIR Capital has done similar ones in Philadelphia and South Carolina. It’s under contract to buy two more hotels along I-35 in Austin. Gordon declined to name those properties.

SHIR Capital is a vertically integrated real estate investment group with 2,200 apartment units in Texas, South Carolina and Pennsylvania.